April 2025 Industrial market report

E-Commerce Growth Fuels Demand for Industrial Space

Updated on April 28, 2025 | 13 minutes read

Key Takeaways:

- E-commerce finished 2024 with $1.19 trillion in total sales, following an 8% year-over-year growth

- Online sales account for 19% of core retail sales, reinforcing the increasing need for warehouse space across the U.S

- National in-place rents for industrial space averaged $8.44 per square foot in March, up 6.7% year-over-year

- New Jersey witnessed the most significant yearly rent growth at 11.3%, while also leading the nation in total sales volume totaling $832 million year-to-date

- Sun Belt markets outpaced port cities in rent growth, with Nashville (10.2%), Atlanta (9.5%) and Miami (9.2%) seeing some of the nation’s highest industrial rent increases

- Orange County reflects strong occupancy levels, with a vacancy rate of only 6.1% at the end of March

Trends & Industry News

E-Commerce Powers Industrial Sector

While tariff uncertainty may create instability for the industrial sector in the near term, e-commerce will continue to drive industrial demand growth during the second half of this decade, according to our industrial property outlook.

The U.S. Census Bureau shows that e-commerce’s slice of the retail sales pie keeps expanding. While core retail sales—which excludes automobiles, their parts and gasoline—grew 3.4% between 2023 and 2024, online sales climbed more than twice as fast. E-commerce grew 8.0% in the year, increasing by $88.5 billion to finish 2024 with $1.19 trillion in total sales.

E-Commerce Sales Volume (Billions)

Online sales’ share of core retail witnessed a continuous growth between 2010—when the Census Bureau began reporting e-commerce data—and the first quarter of 2020, when it sat at 14.1%. The pandemic further accelerated this steady growth, leading to a massive bump in the second quarter of the year, when it hit 20%, followed by the share’s first recorded decline. However, in 2023 and 2024, solid, steady growth returned, and e-commerce accounted for 19% of the core retail sales registered in 2024. As retail sales continue to move online, more industrial space will be needed, according to our industrial market outlook. Estimates place e-commerce sales as requiring about three times as much warehouse space as traditional brick-and-mortar, dollar for dollar.

The decrease in deliveries will allow for existing space absorption and we expect a plateauing of vacancy rates in 2025-2026. That being said, the demand for e-commerce is still strong and aligning for a push in the latter half of the decade.

Peter Kolaczynski, Director, CommercialEdge

No company in the e-commerce space comes close to the size of Amazon or better embodies the pandemic-driven exuberance for industrial space and the pullback that occurred in the following years. Amazon expanded rapidly during the pandemic, acquiring warehouses and vacant land to develop new distribution centers at a blistering pace. Yet by 2022, the company admitted it had overexpanded and paused the opening of some distribution centers while cancelling others and reportedly subleasing some space. Nearly three years after the pullback began, Amazon is looking at expansion once more, according to a Bloomberg report. The e-commerce behemoth has been reportedly reaching out to potential financing partners, exploring a $15 billion expansion across dozens of facilities.

It is important to note, however, that Amazon’s request to capital partners predated President Trump’s Liberation Day tariff announcements and the ensuing trade negotiations. Like many other firms, Amazon may hold off on expansion until there is more clarity around tariffs and trade. Over the long term, e-commerce will remain one of the main drivers of industrial demand. Beyond the dedicated online retailers, traditional big-box retailers like Target and Walmart have been ramping up efforts to compete with Amazon through online sales and omnichannel retail options, both of which will require millions of square feet of additional logistics space over the coming years.

Rents and Occupancy

Sun Belt Markets See Largest Rent Gains

National in-place rents for industrial space averaged $8.44 per square foot in March, up only one cent in the month and 6.7% over the past year.

While New Jersey has seen the highest industrial rent growth over the last twelve months, with in-place rents growing 11.3% year-over-year, the Sun Belt has been the strongest region for rent increases in the last year. In-place rents in Nashville grew 10.2%, while Atlanta saw a 9.5% surge. Moreover, Miami witnessed its in-place rent grow 9.2% and Dallas-Fort Worth saw an 8.5% increase over the last twelve months. Despite port markets having dominated rent gains in recent years, the Southeast has overtaken many of the nation’s top port markets in recent months.

Average Rent by Metro

The national industrial vacancy rate was 8.5% in February, an increase of 30 basis points from the previous month. Vacancies continue to rise, but our industrial market outlook anticipates a plateau sometime in the second half of this year before moving downward again sometime next year. The historic wave of new supply has tailed off, but uncertainty around tariffs has paused many leasing decisions. Once occupiers gain more economic clarity, we expect new leasing activity to pick up. When combined with a slowing new supply pipeline, this will lead to falling vacancies across the nation.

The national spread between a lease signed in the last twelve months and the overall in-place average rent was $1.92 per square foot. The spread decreased 21 cents from the previous month, an indicator of cooling industrial rent growth. The highest spread between the average rent for new leases and the overall market average rent was seen in Bridgeport, where a new lease cost $4.64 more per square foot. Miami ($4.02 per square foot), Seattle ($3.87), New Jersey ($3.81), Charlotte ($3.54) and Boston ($3.51) were the only other markets with a spread higher than $3 per square foot.

Supply

Phoenix’s Pipeline Undergoes Significant Shift

Across the U.S., 345.5 million square feet of industrial space, equal to 1.7% of the total stock, was under construction as of March, according to our industrial real estate report. Construction starts have slowed in recent years but remained elevated compared to pre-pandemic levels. However, that trend may change in 2025 due to increased development costs driven by a 25% tariff on steel and aluminum, since roughly a quarter of the steel and aluminum used in the U.S. is imported.

National Industrial Supply Pipeline Trend (Million Sq. Ft.)

Phoenix continues to have one of the largest new construction pipelines in the country. Even so, that remains significantly below the numbers registered in recent years, and the composition of the pipeline has changed as well. In 2022, an astonishing 39.8 million square feet of warehouse and distribution projects broke ground in Phoenix, accounting for 90% of that year’s new development. At the end of 2025’s first quarter, there were 15.1 million square feet under construction, with nearly two-fifths in data centers (5.8 million square feet). Manufacturing has also been a strong driver in the market, accounting for 22.1 million square feet (16%) of starts this decade. Taiwan Semiconductor Manufacturing Company announced plans to invest an additional $100 billion in its chip-making complex that began production earlier this year.

Transactions

New Jersey Leads First Quarter in Sales Volume

Industrial transactions totaled $11.7 billion during the first quarter of the year, according to our U.S. industrial market report, with properties trading at an average of $125 per square foot.

At the end of March, New Jersey led the nation in industrial transaction volume, with $832 million of sales trading at an average rate of $256 per square foot.

2025 Year-to-Date Sales (Millions)

New Jersey sports strong demand for industrial space due to the population density of the surrounding region and the elevated activity at the Port of New York and New Jersey, one of the nation’s busiest ports. The market’s biggest sale so far this year was Prologis’s $166.8 million acquisition of 201 Middlesex Center Blvd., which sits on more than 30 acres in proximity to Interstate 95. Despite vacancy rates that surpass the national average, the market had the strongest industrial rent growth over the last twelve months. Like most other markets, New Jersey experienced a supply boom in recent years, but slowing development and continued demand will lead to falling vacancies once leasing velocity picks up. Between 2022 and 2024, more than 36 million square feet (5.9% of stock) of new industrial space was completed in the market. Currently, there are just 6.2 million square feet (1.0% of stock) currently under construction.

Western Markets

Resurging Demand Reflected in Orange County’s Low Vacancy and Strong Sales Activity

Orange County remained the tightest industrial market in the West, with industrial vacancy rates at only 6.1%, reflecting strong occupancy levels. In contrast, Denver registered one of the highest vacancy rates in the nation at 9.8% after a 280-basis-point year-over-year surge, highlighting ongoing challenges in absorbing available space. The Central Valley (7.7%), the Bay Area (7.6%) and the Inland Empire (7.3%) also stood below the national vacancy rate of 8.5%, though all three markets saw notable year-over-year vacancy increases—310, 380 and 130 basis points, respectively.

The West continued to be the most expensive region, with most markets’ average in-place rents well above the national rate of $8.44 per square foot. Notably, Los Angeles recorded a significant 7.3% year-over-year increase to reach $15.19 per square foot in March. However, the Inland Empire led the region in rent growth, posting the steepest annual gain of 8.5%, which brought the market’s average rent to $11.09 per square foot. In terms of leases signed in the past 12 months, Orange County saw the highest average rate nationally, at $18.37 per square foot.

West Regional Highlights

Sale prices in nearly every major Western market continued to exceed the national average of $126 per square foot, with Central Valley as the only outlier. At the end of Q1 of 2025, Orange County ($279 per square foot) led the nation in rent prices while also logging one of the biggest sales volumes at $392 million year-to-date. This marked a substantial resurgence from just $57 million a year prior and reflected renewed investor confidence in the market. However, Phoenix topped the region in total industrial sales, totaling $449 million year-to-date.

Phoenix also retained its position as the West’s most active construction market in March, with 15.1 million square feet underway—still a significant drop from the 41.7 million square feet logged the same time last year. Even so, the market still led the region in construction as a percentage of existing stock, at 3.5%. The Inland Empire followed as the second-most active development hub in the West, with 9.8 million square feet under construction, reflecting a modest year-over-year increase from 9.2 million square feet in March 2024. At the opposite end of the spectrum, Orange County continued to trail the region in industrial development, with just 1.1 million square feet underway. However, this marks a noticeable improvement from the 720,000 square feet reported a year prior, signaling a slow but steady uptick in construction activity.

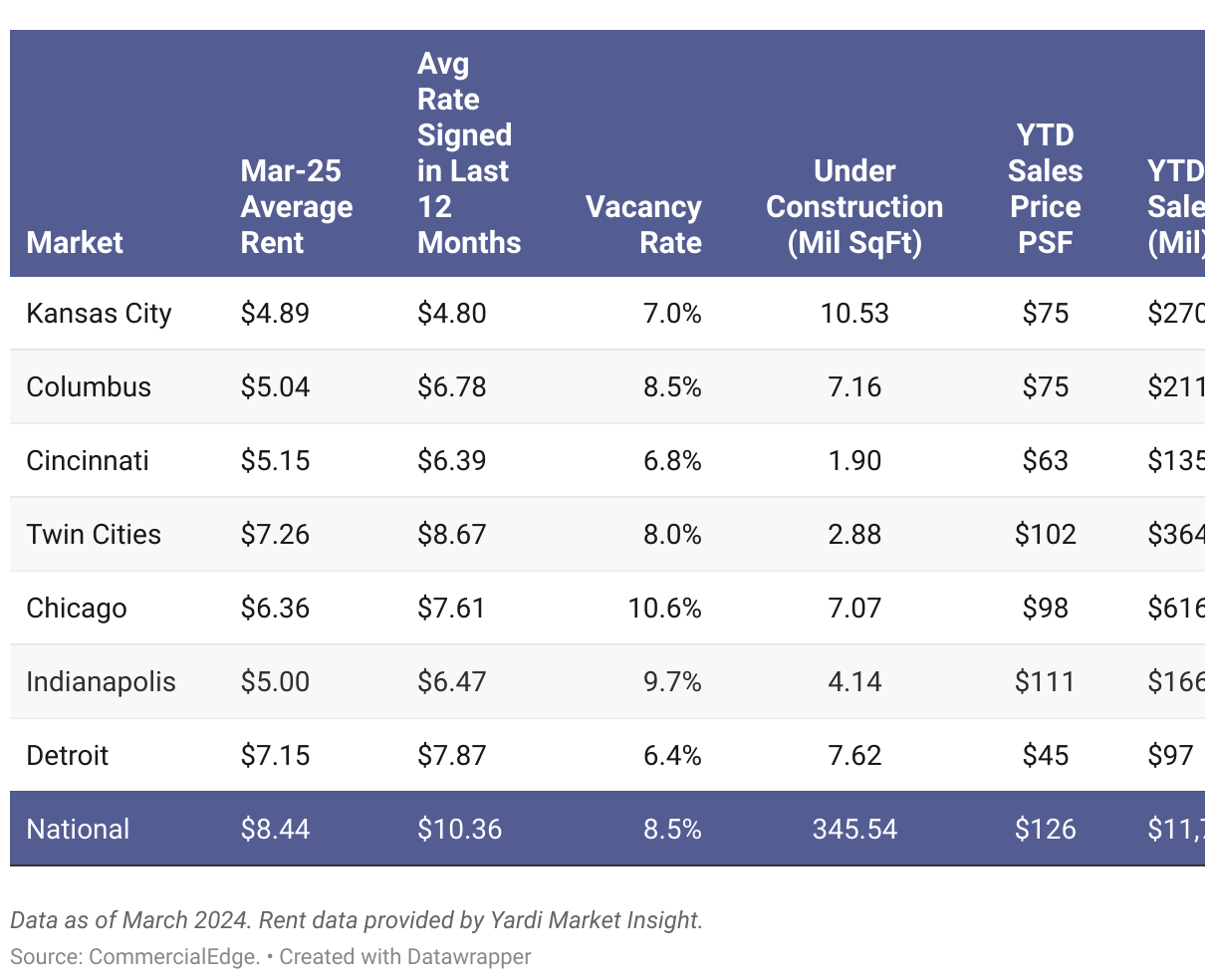

Midwestern Markets

Detroit Sees Highest Occupancy Levels in the Midwest

Detroit stood out among Midwestern markets during March, posting one of the lowest industrial vacancy rates nationwide at just 6.4%. While this represented a 190-basis-point increase year-over-year, the market remained well below the national average of 8.5%, reflecting relatively stable demand. In contrast, other Midwestern hubs continued to face elevated vacancies. Chicago recorded a 10.6% vacancy rate, the second-highest nationwide. Indianapolis followed at 9.7%, driven by a steep 650-basis-point year-over-year increase—one of the sharpest in the region—underscoring persistent challenges in the local industrial landscape.

Sale prices across Midwestern markets continued to lag behind the national average in March, with all markets recording prices below the $126-per-square-foot benchmark. Cleveland posted the most affordable rate in the region, with assets trading at just $39 per square foot. Indianapolis stood out with the highest sale price in the region at $111 per square foot—an impressive jump from $62 per square foot a year earlier. Meanwhile, Chicago retained its position as the Midwest’s top market in terms of sales volume, with $616 million in transactions year-to-date. This represented the third-largest volume nationally despite its average sale price remaining below $100 per square foot.

Midwest Regional Highlights

All Midwestern industrial markets continued to trail the national average rent of $8.44 per square foot, underscoring the region’s affordability. Moreover, none of the Midwestern markets stood above the national rent growth rate of 6.8%. St. Louis and Kansas City remained the most affordable Midwestern markets, with new leases averaging just $4.72 and $4.80 per square foot, respectively. Both metros also saw the tightest lease spreads, suggesting downward pressure on in-place rents.

Kansas City led the Midwest in industrial development during March, with 10.5 million square feet under construction—among the largest pipelines nationally. This represented 3.5% of the total market inventory, placing the metro second among major industrial markets in terms of construction as a percentage of stock. Chicago ended the first quarter of 2025 with a total of 20.1 million square feet of construction starts, which is half the amount of industrial space under construction registered after the first quarter of 2024. The opposite was noted in the Twin Cities, where 3.2 million square feet of construction starts marked the end of March 2024, as that number surged significantly to 8.9 million square feet at the end of 2025’s first quarter.

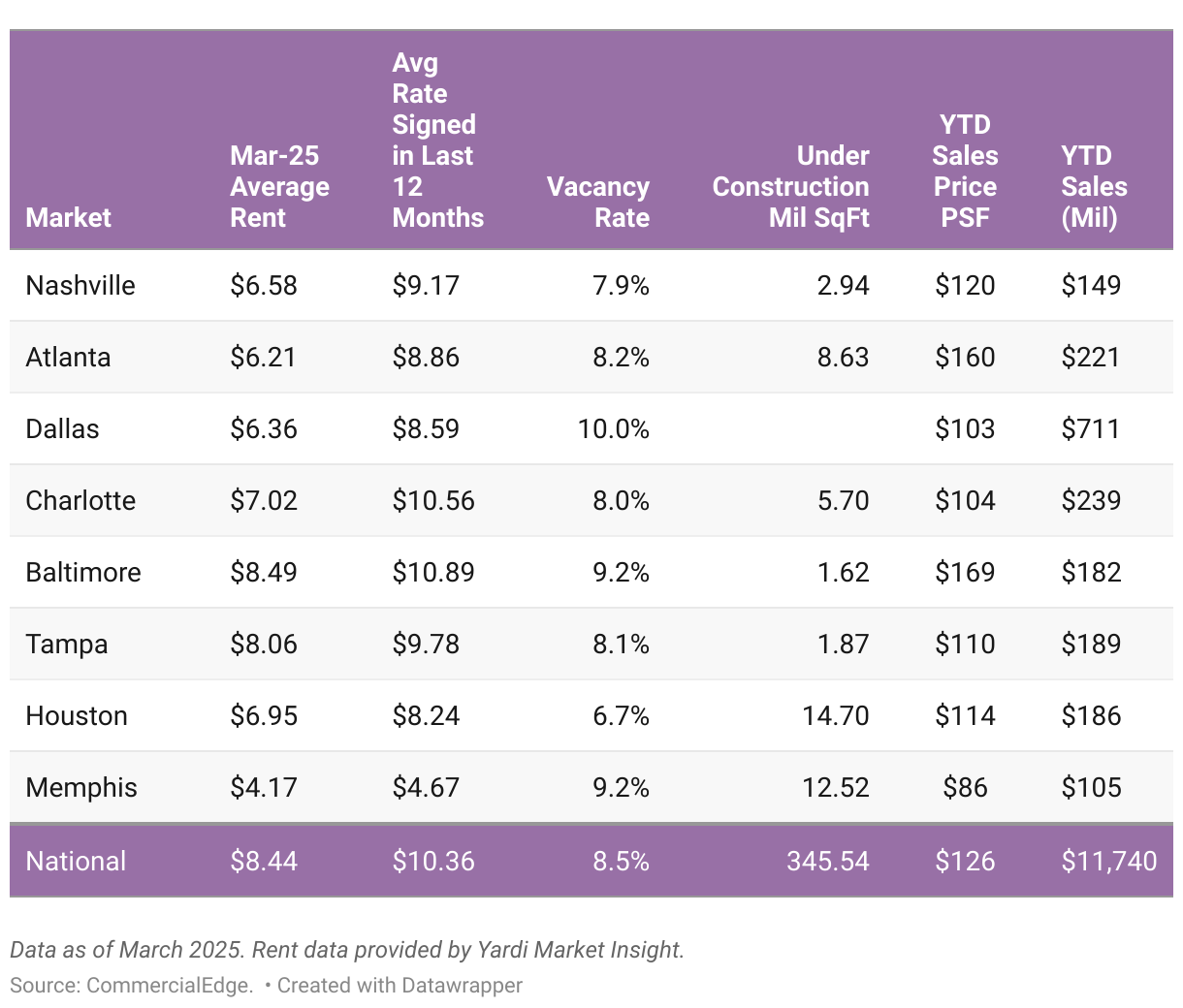

Southern Markets

Memphis Boasts the Nation’s Cheapest In-Place Rents

Memphis ranked as the most affordable market in the nation in March, with in-place rents averaging just $4.17 per square foot and new leases signed at $4.67—both well below the national benchmarks. At the opposite end, Miami emerged as the South’s most expensive industrial market, with in-place rents reaching $12.54 per square foot. The market also recorded one of the widest lease spreads nationally, at $4.02, as recently signed leases climbed to $16.56 per square foot—indicating elevated demand and rising rent pressure. Baltimore was the only other Southern metro to surpass the national average, with in-place rents at $8.49 per square foot.

Baltimore also remained the most expensive industrial market in the South for investment, with assets trading at $169 per square foot. Atlanta also exceeded the national average of $126 per square foot, posting a $160 sale price. Industrial assets in other Southern markets traded at more modest prices, with Memphis recording the lowest at $86 per square foot. Despite maintaining a sale price below the national average, Dallas-Fort Worth stood out by ranking second nationwide in year-to-date sales volume at $711 million.

South Regional Highlights

However, Dallas–Fort Worth continued to be one of the nation’s most challenged markets, posting a 10% vacancy rate in March, the fourth-highest nationwide. Baltimore and Memphis followed closely, each recording vacancies of 9.2%, above the national average of 8.5%. Charlotte experienced the most notable vacancy surge in the region, with its rate climbing 440 basis points year-over-year to 8%. In contrast, Houston maintained one of the lowest vacancy rates nationwide at 6.7% despite a year-over-year uptick of 100 basis points, reflecting sustained occupancy stability in the market.

Dallas–Fort Worth remained the nation’s top industrial development hub in March, with 24.8 million square feet of space underway, followed by Houston and Memphis. Notably, Charlotte’s total under construction and planned projects accounted for 5.3% of the market’s development, the highest share regionally, signaling increased interest for industrial assets in this market. Meanwhile, Memphis stood out with the highest construction as a percentage of stock among major industrial markets, at 4.2%. At the other end of the spectrum, Tampa and Baltimore posted the smallest construction pipelines in the South, with 1.9 and 1.6 million square feet in progress, respectively.

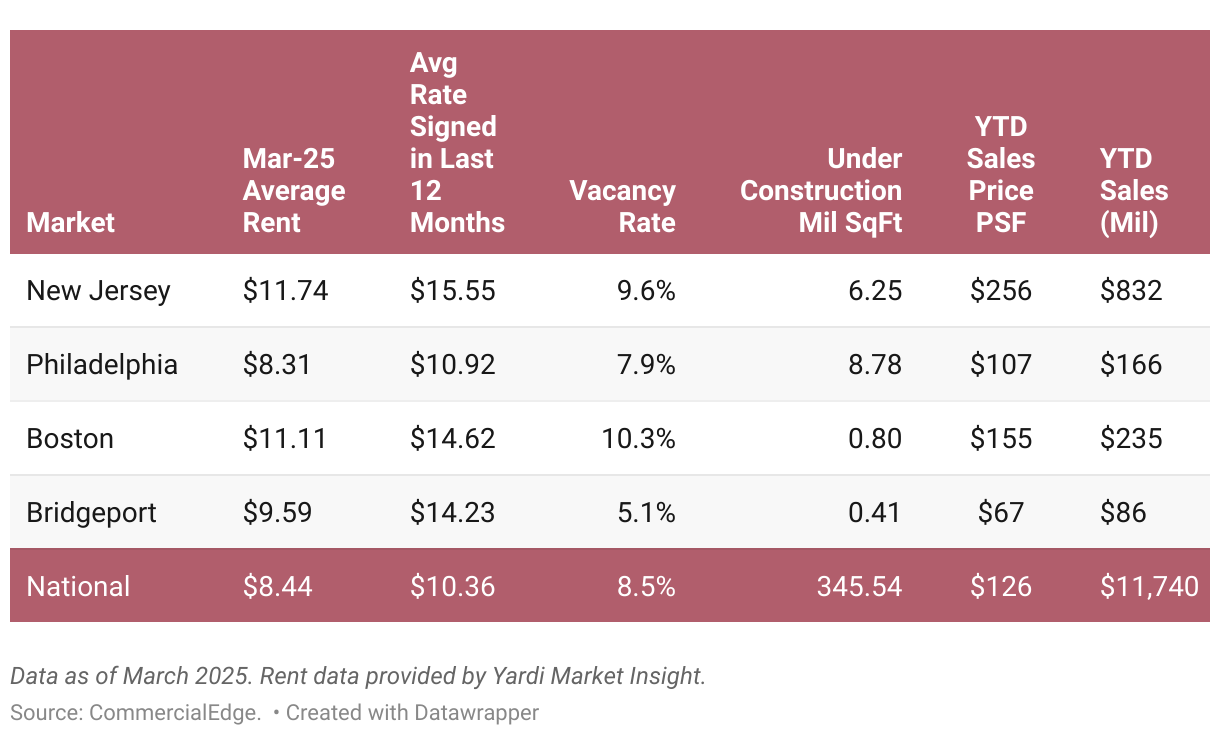

Northeastern Markets

New Jersey Ends Q1 with $832M in Sales Volume

In March, Boston and Bridgeport registered the smallest construction pipelines nationally, with just 800,000 and 410,000 square feet underway, respectively. These figures underscore the sharp contrast in development momentum across the region’s industrial markets. In Boston’s case, this also represents a record low in construction activity since 2019.

The low industrial demand in Boston is also underscored by its vacancy rate —the highest in the region and third nationally —at 10.3% after a 220-basis-point year-over-year increase. Similarly, New Jersey posted industrial vacancy rates of 9.6%, following a substantial 350-basis-point rise, signaling mounting pressure on space absorption. Conversely, Bridgeport emerged as a national standout, boasting the lowest vacancy rate across major U.S. markets at just 5.1%, highlighting the market’s robust industrial demand.

Northeast Regional Highlights

New Jersey led the region with the highest in-place rents, reaching $11.74 per square foot after a significant 11.3% year-over-year increase. The market also recorded one of the widest lease spreads in the nation—$3.81 per square foot—highlighting the sharp rise in rates for newly signed leases. Bridgeport stood out with the widest lease spread nationally at $4.64 per square foot, further emphasizing the growing pricing gap. Boston followed closely behind New Jersey in rental rates, with in-place rents averaging $11.11 per square foot, reinforcing its position as one of the priciest industrial markets in the nation.

New Jersey led the nation in industrial sales volume through the first quarter of 2025, totaling $832 million by the end of March—a sharp increase from the $520 million recorded a year earlier. The market also stood out through its high sale prices, with industrial assets trading at an average of $256 per square foot, the third-highest rate among major U.S. markets. Boston was the only other Northeastern market to exceed the national average, with properties selling at $155 per square foot.

Economic Indicators

Inflation Currently Stable but Expected to Rise

The Producer Price Index (PPI) increased by 2.8% year-over-year in March, dipping under 3% for the first time since November. The gains were mainly driven by the services portion of the index, which grew 3.6% annually. The good portion of the index grew just 0.9% year-over-year in March. On a monthly basis, producer prices fell 0.4%, with goods decreasing 0.9% and services 0.2%.

Economic Indicators

While inflation has cooled from the red-hot levels of three years ago, expectations around it have grown in recent months. Both economists and consumers are now anticipating that tariffs will lead to price increases in the near future. The PPI will be one of the most valuable metrics to track as it is a leading indicator of its more closely followed counterpart, Consumer Price Index (CPI). During both the inflation spike in 2022 and the subsequent cooling that began in 2023, the PPI ran about three months ahead of the CPI. Producers are soon expected to see input prices increase as a result of tariffs and will begin passing them on to consumers.

Download the report

Download the complete April 2025 report for a full picture of how U.S. industrial markets evolved in March, including insights on industry indicators and economic recovery fundamentals.

You can also see our previous industrial reports.

Methodology

The monthly CommercialEdge national industrial real estate report considers data recorded throughout the course of 12 months and tracks top U.S. industrial markets with a focus on average rents; vacancies (including subleases but excluding owner-occupied properties); deals closed; pipeline yield; forecasts; and the economic indicators most relevant to the performance of the industrial sector.

Get access to over 13M commercial property records with regularly verified commercial data, including local market insights, recent transactions and loan details with CommercialEdge Research.

CommercialEdge collects listing rate and occupancy data using proprietary methods.

- Average Rents —Provided by Yardi Market Expert, a cutting-edge service that uses anonymized and aggregated data from other Yardi platforms to provide the most accurate rental and expense information available.

- Vacancy — The total square feet vacant in a market, including subleases, divided by the total square feet of industrial space in that market. Owner-occupied buildings are not included in vacancy calculations.

Stage of the supply pipeline:

- Planned — Buildings that are currently in the process of acquiring zoning approval and permits but have not yet begun construction.

- Under Construction — Buildings for which construction and excavation has begun.

Sales volume and price-per-square-foot calculations for portfolio transactions or those with unpublished dollar values are estimated using sales comps based on similar sales in the market and submarket, use type, location and asset ratings, sale date and property size.

Year-to-date metrics and data include the time period between January 1 of the current year through the month prior to publishing the report.

Market boundaries in the CommercialEdge industrial report coincide with the ones defined by the CommercialEdge Markets Map and may differ from regional boundaries defined by other sources.

Fair Use and Redistribution

We encourage you and freely grant you permission to reuse, host, or repost the research, graphics, and images presented in this article. When doing so, we ask that you credit our research by linking to CommercialEdge.com or this page so that your readers can learn more about this project, the research behind it and its methodology. For more in-depth, customized data, please contact us at [email protected].

Stay current with the latest market reports and CRE news:

Posted in: Industrial, Market Reports

Released on: April 28, 2025